Colorado Capital Gains Tax: What You Need To Know In 2024

Does the Centennial State have a unique approach to taxing profits from investments? Colorado, like many states, levies a capital gains tax, but its structure presents both opportunities and complexities for taxpayers.

Navigating the landscape of capital gains taxation in Colorado requires a clear understanding of the rules and regulations. For years prior to January 1, 2022, certain individuals and entities were eligible for a capital gain subtraction, a provision designed to reduce their tax liability. However, this landscape shifted significantly. For tax years commencing on or after January 1, 2022, the capital gain subtraction is only available to those taxpayers required to file IRS Schedule F, a form primarily associated with farming and agricultural businesses. This change marked a notable adjustment in the state's tax policy, narrowing the scope of those eligible for the subtraction.

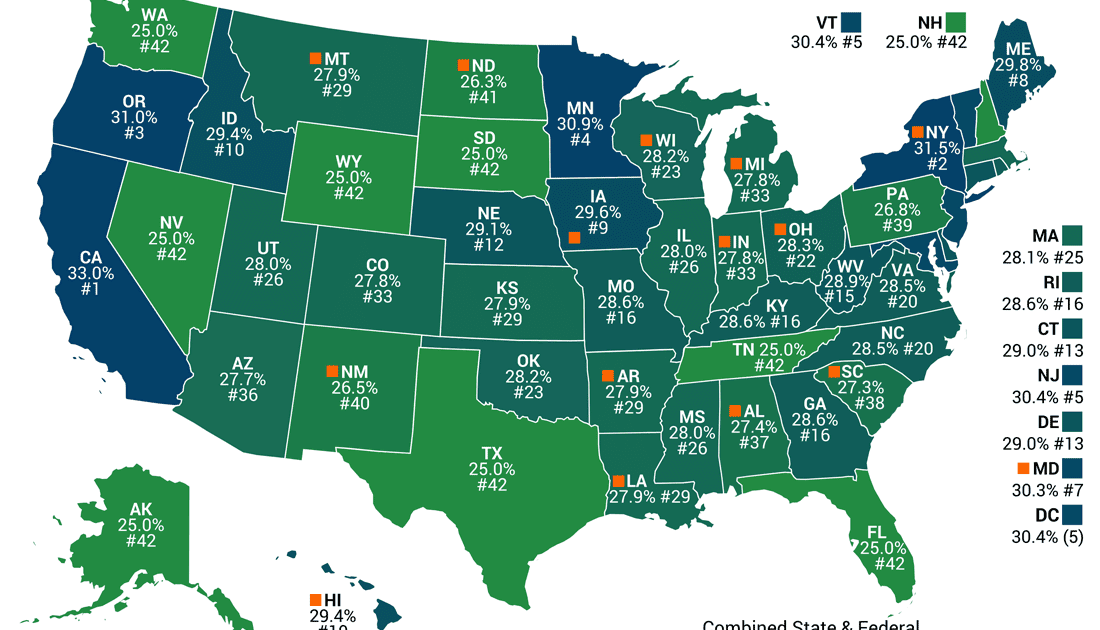

Taxpayers in Colorado are obligated to report capital gains on their state tax returns. These gains are then subject to the state's flat income tax rate. It is crucial to note that as of 2024, this rate stands at 4.4%. This rate has been reduced from the previous 4.55%, a change implemented by Proposition 116 in 2020. These modifications indicate a state government trying to adapt financial landscape for the residents.

| Aspect | Details |

|---|---|

| Tax Rate (2024) | 4.4% |

| Applicable Tax | State Income Tax |

| Tax Base | Capital Gains reported on State Tax Return |

| Eligible for Capital Gain Subtraction (pre-2022) | Individuals, Estates, Trusts, and Corporations |

| Eligible for Capital Gain Subtraction (post-2022) | Taxpayers required to file IRS Schedule F |

| Gains from certain property held 5+ years (may be exempt) | Up to $100,000 |

Capital gains are essentially profits realized from the sale of assets such as stocks, real estate, and other investments. In Colorado, these gains are treated as ordinary income. This means they are taxed at the same rate as regular income, offering a simplified approach to taxation compared to some other states that may have different rates for short-term and long-term capital gains. When calculating your Colorado tax liability, understanding how your adjusted gross income (AGI) is determined is a crucial step. AGI is calculated by taking your total household income and reducing it by certain deductions, such as contributions to your 401(k) or other eligible retirement accounts. From the AGI, you then subtract any applicable exemptions and deductions, whether itemized or standard, to arrive at your taxable income. This taxable income is what the state uses to calculate the capital gains tax.

The sale of your primary residence is another area with unique considerations. A typical homeowner in Colorado selling their primary residence is not usually subject to federal capital gains taxes. The IRS allows a homeowner to exclude up to $250,000 in profits if they are single, or up to $500,000 if they are married filing jointly. This exclusion applies if you have lived in the house for at least two out of the last five years.

Colorado's approach to capital gains taxation is relatively straightforward, with gains being taxed at the standard income tax rate. This flat rate, currently 4.4%, provides a degree of predictability for investors. Compared to other states, this flat rate can be considered moderate. This contrasts with federal capital gains tax rates, which can vary depending on the holding period of the asset and the taxpayer's income level.

While the tax rate itself is flat, other factors can influence the overall tax liability. For instance, the source of the capital gain, whether it is derived from a Colorado source or not, can add layers of complexity. Also, the specific type of asset and the holding period can come into play. Gains from certain property acquired on or after May 9, 1994, and held for at least five years before being sold may be eligible for an exemption of up to $100,000. The Colorado property deduction provides a possible reduction in tax liability for capital gains from real or tangible personal property situated within Colorado. This property should have been acquired between May 9, 1994, and June 3, 2009.

For those seeking tax planning strategies, considering a charitable remainder trust might be one avenue. This can allow you to defer capital gains while supporting charitable causes. While the complexities of capital gains tax regulations are best navigated with the guidance of legal or tax professionals, its important to stay informed about relevant dates and rule changes. For example, for tax years commencing on or after January 1, 2010, there is a maximum capital gain subtraction of $100,000. Remember to verify and consult with financial advisors for updated tax modifications and legal counsel.

The availability of capital gains deductions has also been subject to change. For tax years beginning prior to January 1, 2022, a capital gain subtraction was available to eligible individuals. Starting in 2022, the landscape shifted, with this deduction primarily restricted to those who file IRS Schedule F. This change, driven by evolving tax law and potential state revenue considerations, highlights the need for continual assessment of one's tax situation. The Colorado Department of Revenue provides guidelines that should be consulted for a detailed understanding.

| Aspect | Details | Notes |

|---|---|---|

| Capital Gains Tax Rate (2024) | 4.4% | Flat rate, same as ordinary income. |

| Primary Residence Exclusion | Up to $250,000 (Single), $500,000 (Married Filing Jointly) | IRS rules apply if lived in the house 2 out of last 5 years. |

| Eligible for Deduction (pre-2022) | Individuals, Estates, Trusts, and Corporations | |

| Eligible for Deduction (post-2022) | Taxpayers required to file IRS Schedule F. | |

| Colorado Property Deduction | Available for gains on real/personal property | Property acquired May 9, 1994 June 3, 2009. |

| Maximum Subtraction (for certain gains) | $100,000 | Tax years beginning on or after January 1, 2010. |

The taxation of capital gains in Colorado represents a crucial aspect of financial planning for residents of the state. Understanding the tax rate, the availability of deductions, and specific exemptions allows residents to manage investments in a way that aligns with their financial goals. Whether its the sale of a primary residence or investments in the stock market, knowing the rules in place, can greatly influence how the tax system affects your finances. Consulting tax professionals and advisors, remains the key to successful financial and tax planning.

This article provides a broad overview. Remember, the specifics of your situation may vary. The information provided does not constitute financial, tax, or legal advice. Always consult with qualified professionals for guidance specific to your circumstances.

Disclaimer:This is for informational purposes only and not tax, legal, or financial advice. Always consult with a qualified professional before making financial decisions.